Yes, you can use a prescription discount card with a high-deductible health plan (HDHP). In fact, HDHPs are one of the situations where discount cards deliver their greatest value, because most HDHP holders pay the full retail price for prescriptions until their deductible is met. The discount card reduces that out-of-pocket cost significantly. The main trade-off is that purchases made with a discount card do not count toward your deductible, which matters depending on how close you are to meeting it.

High-deductible health plans have become one of the most common insurance arrangements in the United States, with tens of millions of Americans enrolled through employer-sponsored coverage or the individual market. These plans keep monthly premiums lower in exchange for higher out-of-pocket costs before insurance begins paying. For prescription drugs, that structure means most HDHP enrollees pay the full uninsured retail price for every medication until the deductible threshold is crossed. Prescription discount cards exist precisely to address this kind of cost exposure, and understanding when to use one versus when to run a prescription through insurance is the key decision every HDHP holder should know how to make.

How High-Deductible Health Plans Handle Prescription Costs

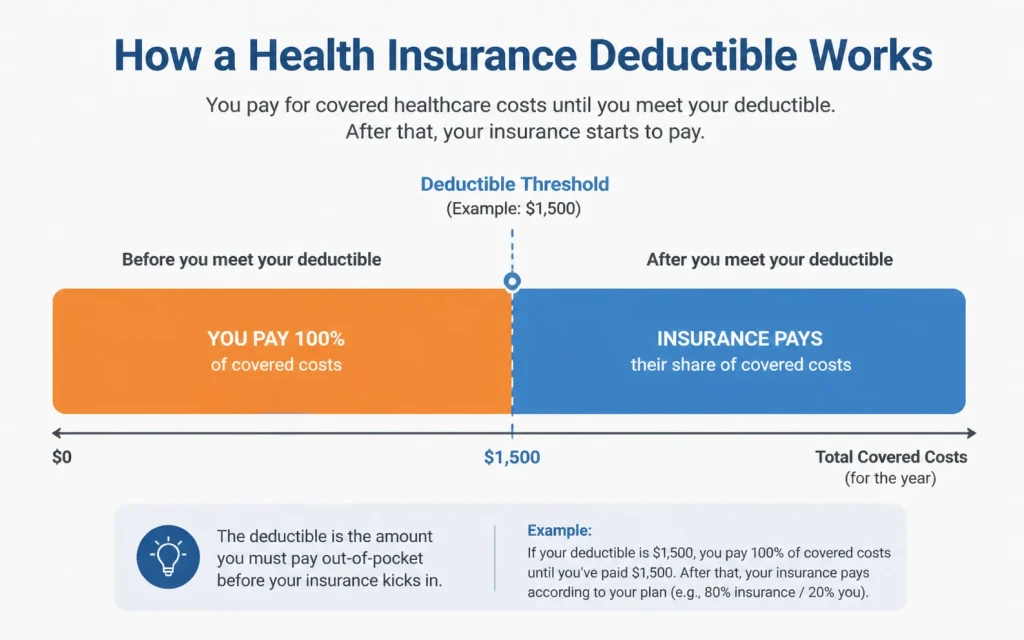

A high-deductible health plan requires you to meet a minimum annual deductible before most insurance benefits kick in. For 2026, the IRS defines an HDHP as a plan with a deductible of at least $1,650 for an individual or $3,300 for a family. Many employer-sponsored HDHPs set deductibles of $2,000 to $5,000 or higher.

Until you reach that deductible, your insurance does not cover most medical expenses, including prescription drugs in most plans. This means that when you hand your insurance card to a pharmacist in January, the system charges you the full contracted rate for that drug rather than a subsidized copay.

That contracted rate is often still lower than the unadjusted retail cash price, but it is rarely the lowest price available. For many common generic medications, a free prescription discount card produces a lower price than what the insurance plan charges before the deductible is met.

Once you cross the deductible threshold, your insurance begins sharing costs and your copays or coinsurance apply. At that point, running prescriptions through insurance is typically the better choice. The strategic question for HDHP holders is: which option costs less right now, given where I am in my deductible year?

When a Discount Card Beats Your HDHP Pre-Deductible Price

Prescription discount cards work by applying a pre-negotiated reduced rate at the pharmacy counter, entirely outside the insurance billing system. Because the card bypasses your insurance entirely, the price you pay is the card’s negotiated rate with that specific pharmacy, not the insurance plan’s contracted rate.

For generic medications in particular, the discount card rate is frequently lower than the insurance contracted rate that applies before a deductible is met. A generic blood pressure medication that your HDHP prices at $38 before the deductible may cost $7 or $9 with a discount card at the same pharmacy. A generic cholesterol medication priced at $55 through your HDHP billing may come down to $12 with the card. These are not hypothetical figures. They reflect the actual spread between insurance pre-deductible pricing and discount card negotiated rates that pharmacists see regularly.

Brand-name medications show a smaller gap. Insurance plans often have negotiated rates on brand-name drugs that can be competitive with or occasionally lower than what a discount card produces, even before the deductible is met. The only reliable way to know which price is lower for any specific drug is to ask the pharmacist to check both at the time of the fill.

Important: Most pharmacies cannot process both a discount card and your insurance on the same transaction at the same time. You choose one or the other per fill. Before finalizing any prescription purchase, ask the pharmacist to tell you the price both ways. This takes less than a minute and is the single most reliable habit for consistently paying the lower of the two available prices.

The Deductible Trade-Off: What You Need to Understand

The core trade-off when using a discount card instead of insurance is that discount card purchases do not count toward your insurance deductible or annual out-of-pocket maximum. Every dollar you spend through a discount card is money spent outside the insurance accounting system.

This matters in two specific scenarios. If you are a patient with high ongoing medical costs who typically meets your full deductible by March or April each year, using a discount card early in the year delays reaching the threshold where insurance begins paying its share. In that case, running prescriptions through insurance at the higher pre-deductible rate may actually be the better financial decision because each fill brings you closer to the point where insurance takes over and your costs drop sharply.

If you are a patient with moderate healthcare needs who rarely or never meets your full deductible in a given year, the deductible consideration is far less relevant. You are going to pay out of pocket for prescriptions all year regardless.

In that case, the discount card price is almost always the better option because you receive immediate savings without any trade-off in insurance benefit accumulation. Managing prescription costs when insurance is not covering your expenses is exactly the situation most HDHP holders face for much of the year.

| Your Situation | Better Choice | Reason |

| Early in the year, far from deductible, light medical costs expected | Discount card | Lower immediate price, deductible unlikely to be reached anyway |

| Early in the year, heavy medical costs expected (surgery, chronic illness) | Insurance billing | Each fill counts toward the deductible, accelerating insurance coverage |

| Deductible already met for the year | Insurance billing | Subsidized copay applies; discount card price is rarely lower |

| Deductible very close but not yet met | Insurance billing | A few more fills may push you past the threshold |

| HDHP pre-deductible price is higher than discount card price for a generic | Discount card | Immediate savings outweigh deductible accumulation for most patients |

| Prescription is not covered by your HDHP formulary at all | Discount card | Insurance offers no benefit; card provides the only available discount |

HSA Compatibility: An Important Rule for HDHP Holders

Many people enrolled in HDHPs also contribute to a Health Savings Account (HSA), which allows pre-tax dollars to be saved and spent on qualified medical expenses including prescription drugs. The IRS rules governing HSAs include one provision that affects how discount cards should be used in the context of an HSA-paired HDHP.

Under IRS guidance, an individual enrolled in an HSA-eligible HDHP generally cannot receive benefits from other health coverage for expenses below the deductible without losing HSA eligibility. A prescription discount card is not classified as health insurance or a health plan under IRS definitions, so using one does not jeopardize your HSA eligibility in most circumstances.

However, there is a nuance worth confirming with your plan administrator or tax advisor. Certain employer-sponsored arrangements layer additional prescription benefit structures on top of an HDHP in ways that can create HSA compatibility concerns. If your employer’s plan includes a separate prescription benefit that kicks in below the deductible, confirm whether using a discount card on the same prescription creates any interaction with that structure before assuming the standard rule applies to your specific plan.

For the vast majority of standard HDHP holders without layered prescription benefits, using a discount card is straightforward and compatible with maintaining an HSA. You are simply paying cash at a negotiated rate rather than billing insurance, which the IRS treats as a standard out-of-pocket expense.

How to Decide on Every Fill

The practical framework for every prescription fill as an HDHP holder is a two-question process that takes under two minutes at the pharmacy counter.

First, ask the pharmacist: “What is the price if I run this through my insurance?” This gives you the pre-deductible contracted rate or, if you have already met your deductible, your standard copay.

Second, ask: “What would the price be with a discount card?” This gives you the card’s negotiated rate at that specific pharmacy.

Compare the two numbers. Pay the lower one. That is the entire decision process. Identifying the pharmacy where that card rate is most competitive adds a third dimension for new or high-cost prescriptions, since the same card produces different prices at different pharmacy locations, and a five-minute price comparison call before filling a new prescription consistently produces better results than filling at whichever pharmacy is most convenient.

For ongoing chronic prescriptions where the prices are stable and predictable, you can make this evaluation once and then apply the same approach to every subsequent fill without repeating the comparison each time. If your insurance plan or the pharmacy’s pricing changes at any point, run the comparison again to confirm which option is still better.

The NuLifeSpan Rx Discount Card: Built for HDHP Holders

For the months of the year when your HDHP deductible has not been met, the NuLifeSpan Rx prescription discount card is the most direct tool for reducing what you pay per fill. It is completely free, never expires, requires no sign-up, and is accepted at over 35,000 pharmacies nationwide. It delivers savings of up to 80 percent on thousands of covered medications and works for both human and veterinary prescriptions at participating locations.

Ask the pharmacist to run your next prescription both ways before finalizing, and present the NuLifeSpan Rx card if the discounted price is lower. For most generic medications before the deductible is met, it will be.

Other Savings Strategies That Pair Well with HDHPs

A discount card is the first and most accessible tool for HDHP holders, but it works best as part of a broader approach to managing prescription costs during the pre-deductible months.

Switching to generic equivalents wherever clinically appropriate compounds the savings from a discount card because generics are already priced significantly lower than brand-name drugs before any card is applied. The combination of a generic substitution and a discount card produces the lowest achievable price at most pharmacies for most common maintenance medications. Understanding why brand-name drug prices remain so high reinforces why the generic switch is always worth discussing with your prescriber for any long-term prescription.

Requesting a 90-day supply for stable chronic medications reduces the per-dose cost further and decreases the number of trips required per year. Most pharmacies offer a lower per-unit price on a 90-day fill than on three separate 30-day fills of the same drug. Navigating the pricing and supply options available at major retail pharmacies helps you maximize both the discount card benefit and the bulk-supply benefit simultaneously.

Manufacturer patient assistance programs and copay cards are worth exploring for brand-name medications without generic equivalents. These programs can reduce or eliminate the cost of eligible brand-name drugs for patients who meet income or insurance criteria, and they operate independently of the insurance billing system in ways that are generally compatible with HDHP and HSA arrangements for most standard plan structures.

What to Do When Your Deductible Resets in January

The financial exposure of an HDHP is most acute at the beginning of each new benefit year, when the deductible resets to zero and every prescription fill is again charged at the pre-deductible rate. January through March is the period when HDHP holders most frequently experience sticker shock at the pharmacy counter, and it is the period when discount cards deliver their most consistent value relative to insurance billing.

The most practical preparation is to check the discount card price for every prescription you fill regularly before the year resets and compare it against your plan’s pre-deductible rate for those same medications. Pharmacy prices shift periodically, so rechecking at the start of each benefit year confirms whether the card or insurance billing is still the better option for each drug in your regular regimen. Doing this once in December or early January sets you up for a full year of informed decisions without needing to repeat the evaluation at each individual fill.

NuLifeSpan Rx Pet Prescriptions: HDHP Savings Logic Applies to Your Pets Too

Pet insurance deductibles work similarly to human HDHPs, and veterinary clinic prescription pricing has no regulatory ceiling whatsoever. The NuLifeSpan Rx pet prescriptions savings program gives pet owners access to the same free discount card for veterinary medications at participating retail pharmacies. Ask your vet for a written prescription, fill it at a retail pharmacy with the card, and pay a fraction of the clinic price on every refill.

Frequently Asked Questions

Can I use a prescription discount card while enrolled in an HDHP?

Yes. A prescription discount card is accepted at most retail pharmacies for any valid prescription regardless of your insurance status or plan type. Being enrolled in an HDHP does not restrict your ability to use a discount card. The card simply routes the transaction as a cash purchase at a pre-negotiated rate rather than billing your insurance. For most generic medications before your deductible is met, the discount card price is lower than the pre-deductible insurance rate, making it the more cost-effective option in those situations.

Does using a discount card affect my HSA eligibility?

In most standard cases, no. A prescription discount card is not classified as health insurance or a health coverage plan under IRS definitions, so using one does not jeopardize HSA eligibility for most HDHP enrollees. You are simply paying cash at a negotiated rate, which the IRS treats as an ordinary out-of-pocket expense. The nuance applies if your employer’s plan includes a separate prescription benefit that provides coverage below the deductible, which could create an HSA compatibility issue. If you are unsure whether your specific plan has this structure, confirm with your HR department or a tax advisor before assuming the standard rule applies.

Will discount card purchases count toward my deductible?

No. When you use a discount card, the transaction bypasses your insurance billing system entirely. The amount you pay does not count toward your deductible, annual out-of-pocket maximum, or any other insurance accumulator. This is the primary trade-off to understand when deciding between a discount card and insurance billing for any given fill. For patients who rarely or never meet their full deductible, this trade-off is largely irrelevant because the deductible threshold would not have been reached regardless. For patients who typically meet their deductible by midyear, the decision requires more careful evaluation of immediate savings versus deductible accumulation.

How do I know whether the discount card price or my insurance price is lower?

Ask your pharmacist to check both before finalizing any transaction. Most pharmacy systems can display both your insurance pre-deductible contracted rate and the discount card rate within seconds. You compare the two numbers and pay the lower one. For generic medications, the discount card price is frequently lower than the insurance pre-deductible rate. For brand-name medications, the relationship is less predictable and varies by drug, plan, and pharmacy. Making this a routine two-question habit at every fill ensures you are never paying more than necessary.

What happens to my discount card savings once my deductible is met?

Once your deductible is met and your insurance begins paying its share, your standard copays or coinsurance apply. At that point, your insurance copay is typically lower than the discount card price because insurance is now actively subsidizing the cost. For most patients who have met their deductible, switching back to billing through insurance for the remainder of the benefit year makes the most financial sense. The discount card becomes useful again at the start of the next benefit year when the deductible resets.

Are there medications where the discount card is always better than an HDHP pre-deductible price?

For common generic medications, the discount card price is better than the HDHP pre-deductible price in a large majority of cases. Drugs in categories like blood pressure management, cholesterol reduction, type 2 diabetes, thyroid conditions, and mental health maintenance have strong generic availability and extremely competitive discount card pricing, often under $15 for a 30-day supply. For brand-name medications without generics, the comparison is less predictable and must be evaluated individually. The only way to confirm which is lower for any specific drug is to ask the pharmacist to run both options before committing to either.

Can I use a discount card for specialty or high-cost medications with an HDHP?

You can use a discount card for specialty medications at pharmacies that carry and dispense them, but the savings profile differs from standard medications. Specialty drugs often have their own manufacturer copay assistance programs that reduce the cost more substantially than a general discount card, and those programs are worth exploring before defaulting to any card. Some specialty medications are only dispensed through specialty pharmacies that may not participate in standard discount card networks. For high-cost medications, contacting the manufacturer’s patient support line directly to ask about available savings programs is the most thorough first step.

Can I pay for discount card prescription purchases with my HSA funds?

Yes. Prescription medications are qualified medical expenses under IRS rules, and you can use HSA funds to pay for them regardless of whether the purchase is billed through insurance or paid as a cash transaction with a discount card. The prescription itself is what qualifies the expense, not the payment method used. Keep the pharmacy receipt for any HSA-funded discount card purchase as documentation of a qualified medical expense in case of an audit.

Does the discount card work the same way at every pharmacy?

The same card produces different prices at different pharmacy locations because the negotiated rates in the card’s network are pharmacy-specific. The NuLifeSpan Rx card may price a particular generic at $8 at one pharmacy and $14 at another location two miles away. This is why comparing the card price at two or three pharmacies before filling a new or high-cost prescription consistently produces better results than filling at whichever location is most convenient. For established chronic prescriptions where you already know the pricing, this comparison only needs to be done once and then revisited at the start of each new benefit year.

Is a discount card useful if I have an HDHP with a prescription benefit that applies before the deductible?

Some HDHP plans include a separate prescription benefit that covers certain drugs, particularly generics, at a defined copay before the full medical deductible is met. If your plan has this structure, the prescription benefit copay and the discount card price should both be checked and compared. For drugs covered under the prescription benefit at a low copay, the insurance benefit may already be delivering a price that is difficult to beat with a card. For drugs not covered under that separate benefit, or for drugs where the copay is still higher than the card price, the discount card remains a valid and often better alternative.

Conclusion

Prescription discount cards and high-deductible health plans are not in conflict. They are tools that serve the same person at different points in the benefit year. Before the deductible is met, a discount card frequently reduces what you pay per fill to a lower level than your HDHP’s pre-deductible contracted rate, particularly for generic medications. Once the deductible is met and insurance begins subsidizing costs, billing through insurance is typically the better option. The decision framework is simple: ask the pharmacist to check both prices before finalizing any transaction and pay the lower one.

The only meaningful trade-off is that discount card purchases do not accumulate toward your deductible, which matters if you are on track to meet it before year end. For the majority of HDHP holders who never fully meet their deductible in most years, this trade-off is largely irrelevant and the discount card is the straightforwardly better option on most fills. Visit the NuLifeSpan Rx blog for more guides on managing prescription costs under every type of insurance arrangement.

{kind=link}